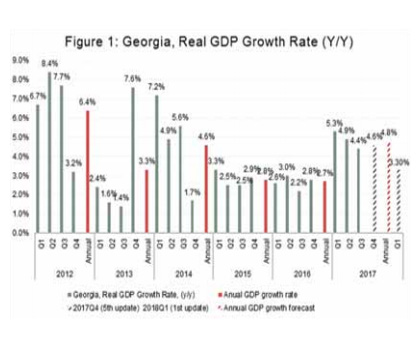

ISET-PI updated its forecast of Georgia’s real GDP growth rate for the fourth quarter of 2017, and the first quarter of 2018. Here are the highlights of this month’s release:

• Geostat updated its preliminary estimate of real GDP growth for the first and second quarters of 2017. The Q1 and Q2 GDP growth estimates were revised upward by 5.3% and 4.9%, respectively (0.2% higher than initial estimates). The third quarter estimates remained unchanged so far.

• Real GDP growth rate reached 5.7 % y-o-y for October 2017. As a result, estimated real GDP growth for the first ten months of 2017 was 4.9%.

• ISET-PI’s real GDP growth forecast for the fourth quarter of 2017 remained at 4.6%.

• Based on September’s data, we expect the annual growth in 2017 to be 4.8%.

• ISET-PI forecasts GDP growth for the first quarter of 2018 to be 3.3%.

Between the months of September and October, very few variables changed in a meaningful way. The most significant changes were observed for variables related to national and foreign currency deposits, money supply (currency in circulation), excessive inflation (inflation that exceeds targeted level), and external statistics.

External Sector: positive trends in exports and trade balance, but not yet at the level of 2014

The first three quarters of 2017 were characterized by improved economic activity in Georgia’s neighboring countries.

The Armenian economy advanced 7.0%, 5.5%, and 3.5% y-o-y in the first three quarters of 2017, respectively, and according to the National Statistical Service of the Republic of Armenia (Armstat), the real GDP growth figure was even more impressive in the month of October, reaching the 17.6% mark. Russia’s quarterly growth rates are also exhibiting an upward trajectory this year.

The Turkish economy grew by 11.1% y-o-y in the third quarter of 2017, accelerating sharply from the 5.4% expansion in the previous three-month period. This was the strongest pace of expansion since the third quarter of 2011, boosted by household consumption, fixed investment, exports, and government spending (Trading Economics). Azerbaijan is the only country in the region that was still was still in the grip of a recession.

In the first two quarters of 2017, the economy of Azerbaijan contracted by 2.7% and 2.8%, respectively (see Figure 2).

Improved economic activities in the region increased the demand for Georgian goods and services. Thus, Georgian exports continued to expand, increasing by 39% relative to the same month of the previous year. Moreover, import of goods and services increased moderately by 10% yearly, and as a result, the trade balance (net-exports) improved by 0.9% (trade deficit reduced by 468 million USD).

Unfortunately, trade variables are recovering from a very low base, and, despite the rapid growth, neither exports nor total trade have managed to reach their 2014 level just yet (level before regional crisis – see Figure 3).

An increase in remittances and tourism further contributed to higher growth estimates. Remittances went up by 20% compared to the same month of the previous year, while the number of tourists increased by 19.9% yearly. Furthermore, there was a dramatic increase in the number of visitors in October (15% yearly growth). This suggests an expected increase in Georgia’s services exports. Overall, an improved trade balance, increased money inflows, and a dramatic rise in the number of visitors and tourists in October had a significant positive impact on our growth forecast.

National and Foreign Currency Deposits: long maturity deposits decline

As far as ISET-PI’s forecast model, the first group of variables that changed significantly in October were the national and foreign currency deposits in commercial banks. Almost all types of deposits increased significantly both in yearly and monthly terms. The only category of deposits that experienced a yearly decline was, again, the Time Deposits with maturity of more than 12 month in national and foreign currency. These variables went down by 17% and 18%, respectively, year on year. Since deposits with long term maturities are one of the most important sources for country investment, their decline had a negative effect on the model’s growth estimate.

Furthermore, the Dollarization Ratio of the total non-bank deposits increased by 1.0%, up to 66.4%. The Dollarization Ratio of the total credit portfolio, however, was reduced by 0.8%, and amounted to a much lower 57.3%. These trends signal an increase in currency mismatch on the commercial banks’ balance sheets, and may exacerbate currency risks.

In brief, despite the promising trends in the accumulation of national and foreign currency deposits, the overall effect of all deposit-related variables on the growth forecast was quite limited.

Money supply is expanding

The other set of variables that had a significant positive effect on our forecast were related to the currency in circulation. In October 2017, the annual growth rate of loans issued by commercial banks amounted to 24.6%. Even without the exchange rate effect, the annual growth of bank loans was 15.7%. All the monetary aggregates, including the largest Broad Money (M3), increased significantly (by 3% monthly and 18% yearly) in the corresponding month. The largest yearly increase was observed again for Monetary Aggregate M2, which increased by 22% relative to the same month of the previous year. Moreover, Currency in Circulation (CCIR) itself increased by 13% in yearly terms.

Higher inflation is putting a brake on growth

According to our model, the main negative contributor to the growth estimate was increased consumer prices compared to the same month of the previous year. Several factors contributed to rising price levels: First, at the end of October, the lari depreciated with respect to the US dollar and euro (by 4% and 3% respectively, compared to the end of the previous month), which fueled expectations of further depreciation (these processes tend to have a self-fulfilling nature), and exacerbated the upward pressure on prices (since depreciation leads to an increase in imported product prices, which the raises overall price level in the country). Second, world prices for oil, as measured by Europe Brent Spot Price FOB, increased by 2% monthly and 16% yearly, which also put an upward pressure on the general price levels in Georgia Third, the effect of the one-time increase of the excise tax has not been exhausted yet. Thus, an increase in the inflation rate reduced the purchasing power of consumers, and further hindered economic growth.

Our forecasting model is based on the Leading Economic Indicator (LEI) methodology developed by the New Economic School, Moscow, Russia. We constructed a dynamic model of the Georgian economy, which assumes that all economic variables, including the GDP itself, are driven by a small number of factors that can be extracted from the data well before the GDP growth estimates are published. For each quarter, ISET-PI produces five consecutive monthly forecasts (or “vintages”), which increase in precision as time goes on. Our first forecast (1st vintage) is available about five months before the end of the quarter in question. The last forecast (5th vintage) is published in the first month of the next quarter.

Davit Keshelava and Yasya Babych

Georgia Today