Unlike most commodities that are provided by private actors competing with each other, a currency is provided by a monopolist. The only institution that is allowed to produce laris is the National Bank of Georgia (NBG).

The task of the NBG-monopolist is made difficult by various peculiarities that cannot be found in other markets. First of all, lari once injected into the economy are not consumed or used up. They remain in the economy “until the cows come home”, as they say in Scotland. This is starkly different to what we observe in most other markets. If bakeries interrupt their production of bread, after a short period of time the bread that was circulating around is eaten. Then the ratio of supply and demand in the market decreases and the bread price increases. In contrast, if the National Bank of Georgia stops printing money, the amount of money circulating around remains the same. Hence, it is very costly for the NBG to reduce the supply of money, as this does not mean that the “production of lari” has to be interrupted but lari have to be bought back, depleting scarce foreign currency reserves.

On the other hand, an ordinary monopolist typically faces production costs, and in this respect the NBG has an easier life. It is almost costless to increase the supply of money by starting the printing press.

SHOULD THE NBG STEP IN?

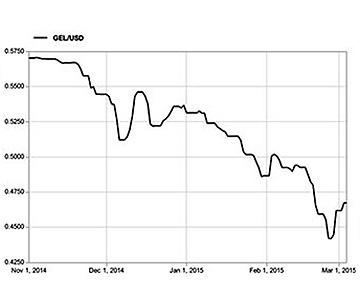

Many Georgians were unsettled by the sharp depreciation of the lari vis-а-vis the dollar that occurred within the last months. Indeed, as the graph shows, since the beginning of November 2014 the value of the lari, measured in dollar, moves constantly downwards. On the first of November one could buy one lari for approximately 57 dollar cent in international currency markets, while today one has to pay only about 47 dollar cent (about a week ago the situation was even worse, when a lari was traded for just 44 dollar cent). In relative terms, moving from 57 cents to 47 cents is a devaluation of almost 20%.

There was a lively discussion about whether the NBG should use its foreign currency reserve “ammunition” for buying back lari and thus reducing the supply. Such an intervention was demanded by Georgian politicians, but history is full of examples which show that it almost never works. Faced with international exchange rate dynamics, central banks, even if much bigger than the NBG, are largely helpless. It is a war that cannot be won, and the foreign currency reserves get lost underway.

In January 2014, the Russian central bank held more than 500 billion dollars in foreign currency, and to this day they used approximately 120 billion dollars to buy back rubles. Yet did it help? From January 2014 to today the ruble lost approximately 50% of its value, much more than the lari in the same time. Even the Russian central bank, really having a lot of foreign currency in store, is impotent in view of the massive loss of trust in the ruble throughout last year.

When there are fundamental downward forces, interventions on part of the central bank can usually delay or slow down the depreciation for some time, but it is worth the money? A famous case is the Mexican peso crash in 1995. When the peso came under pressure, many US pension funds were engaged in Mexico, and they feared a loss in the value of their (financial) investments made across the border. Political pressure was exerted on the Mexican central bank to delay the peso crash, and Mexico was provided with a multi-billion dollar bailout package. These measures, however, die not prevent the overall depreciation of the peso – it was just delayed, giving the US investors the necessary time to disengage. The episode was not to the advantage of Mexico, as later they had to pay back the bailout package given to them, while their currency had crashed nonetheless (a detailed account of this and similar cases can be found in Lester C. Thurow’s The Future of Capitalism, Nicholas Brealy 1997).

Even more problematic would it be to peg the lari to the dollar in a fixed exchange rate regime. This would invite currency traders to apply their standard speculation scheme. Worldwide, they could coordinatedly borrow lari in huge amounts and then sell these borrowed laris for dollars at the fixed exchange rate. The central bank guarantees the exchange rate, so it has to sell dollars for lari. Yet in the process, the foreign currency reserves of the central bank melt away, and at some point the central bank would run out of reserves and could not buy further lari. At that point, the lari crashes, allowing the speculators to buy back the laris they owe to their creditors for just a fraction of the dollar price they had received when selling the laris previously. If the central bank really defends to the bitter end but is finally defeated, all its currency reserves are pocketed by the speculators. Even the heavy-weight Bank of England fell victim to this scheme, when in 1992 they had pegged the British pound to a basket of other European currencies, mainly the German mark. Despite trying to defend their exchange rate, they were finally defeated, and in the process transfered huge amounts of money to speculators, among them George Soros who made about one billion dollars in this attack against the pound.

To sum up, there is not much what one can do on the supply side of lari. If one wants to support the exchange rate, one has to stimulate demand. Yet as it turns out, this is also not easy.

WHY DO PEOPLE (NOT) DEMAND LARI?

The three classical functions of money are medium of exchange, store of value, and unit of account (see, for example, Burda and Wyplosz’ Macroeconomics: A European Text, Oxford University Press 2005). While the last function does not drive demand for money, the first two are relevant for how much lari (or any other currency) people want to hold. If one plans expenditures in lari, be it for investments in Georgia or just buying Georgian products, one needs to have lari.

Some people have argued that there is less demand for lari because the investment climate in Georgia has deteriorated. This is countered by those who say that foreign investments did in the past not account for a large share of the demand for lari, and hence investor confidence could not play a big role in the lari depreciation.

However, it is difficult to say how the price of the lari reacts to a change in demand. Perhaps, having a little more investor confidence and therefore a little more demand for lari would make a considerable difference in the price. Moreover, the demand for laris is not governed by past activities but by future plans and expectations about Georgia’s economic wellbeing. If people demand lari as a medium of exchange, they plan to do transactions in the future, and the medium of exchange purpose of money is all about future transactions. Statistics of the past do not capture these expectations.

If one wants to make the lari attractive as a medium of exchange, there is not so much one can do, yet a sound economic policy which creates a good investment climate would be advantageous. Some policy measures of the last two years, like the new immigration law, were not helpful in this respect. In this context, it is important to keep in mind that an economy which heavily depends on foreign investment is much more sensitive to policy mistakes. In Germany, they recently introduced a minimum wage which came with ridiculous bureaucratic requirements (employers have to write down the exact time, minute by minute, at which each employee works), and there is a plethora of other economically questionable decisions that are made in Germany in every year. Yet Germany’s economy is diversified and strong, and it takes many mistakes to bring the economy down (not to say that this will not happen at some point). Georgia, however, mainly depends on foreign capital and is therefore much more fragile. The decision not to invest in Georgia is a rather easy one, given that there are many comparable countries competing for investor money.

Finally, the medium of exchange purpose of the lari is related to what people expect they can buy with these lari, i.e. what and how much the Georgian economy will produce in future. Growth prospects depend on reasonable economic policies, and one may wonder whether the last two years were used optimally to foster growth in Georgia.

However, the biggest driver of the lari depreciation is the fact that people do not perceive lari anymore as a good way to store their value. This is of course interconnected with the medium of exchange purpose – if there will be many people demanding lari for future transactions, lari will be a reasonable way to store one’s value.

There is a global movement towards storing one’s value in dollar, illustrated by the fact that not only the lari depreciated but also many other currencies of developing economies. From October 2014, the Armenian dram devaluated by around 16%, the Turkish lira by around 11%, and the Azerbaijani New Manat, which until recently was defended bravely by the Azerbaijani central bank, just in the last few days lost more than 20% of its value. The differences in these values may be due to different investor confidence and future expectations, yet by and large it is a global trend beyond the control of a small country like Georgia.

This shift in preferences to not store so much value in lari anymore is like a natural desaster. One can hope that the crises in Ukraine and Russia as well as other geopolitical threats will lose intensity, but as long as Georgia’s economy is in a fragile state, which it will be for decades to come, it will be exposed to the capers of the global economic climate. The only safe harbor would be to join the Euro area.

Florian Biermann

Georgia Today